As this year came to the end, December represents a strategic turning point for businesses operating in the digital market. It is precisely during this period that companies consolidate their 2025 results, assess performance across the final quarter, and extract meaningful insights to recalibrate their strategies for the year ahead.

Conducting a structured and data-driven analysis of 2025 is therefore not only essential to understand what worked and what did not, but also to anticipate the economic and technological dynamics that will shape 2026. In an increasingly competitive and regulation-driven digital ecosystem, the ability to translate past performance into future readiness will be a key differentiator.

Given the vastness of the digital economy, this report focuses on four core areas that most clearly defined the market evolution during 2025:

The advertising world during 2025 adapted to major changes driven mainly by technological advancements and economic shifts but declined also by related regulations that became stricter. For all app creators who want to stay competitive in the market and gain the most from their marketing budgets, understanding these current trends become essential.

Digital advertising, independently from the market we are analysing, continues to dominate with its share of global ad spend projected to hit 75.2%, totaling $777 billion worldwide in 2025. Interesting to highlight the high volume of digital advertising spending exclusively located in the US that is expected to reach $466.34 billion by the end of the year.

On one hand we must highlight that search and retail media are seeing a very profitable growth with ad spend in these areas rising 10% to $167 billion. The same increasing ad spend direction trend is also visible in Social MediaAnother,a sector that counts an increase of 11% to $92 billion.

On the other hand, instead the traditional media has been more negatively affected by technological advancements. Many marketers in fact are switching from TV channels toward digital platforms, characterised surely by better targeting and more efficient measurable results.

AI has shifted from a future-facing concept to a present everyday solution for marketing operations and its application is one of the most noteworthy trends of this year. In 2025, marketers rely on artificial intelligence for both operational and strategic tasks across user acquisition, creative production ,CRM (Customer Relationship Management) systems and campaign optimization.

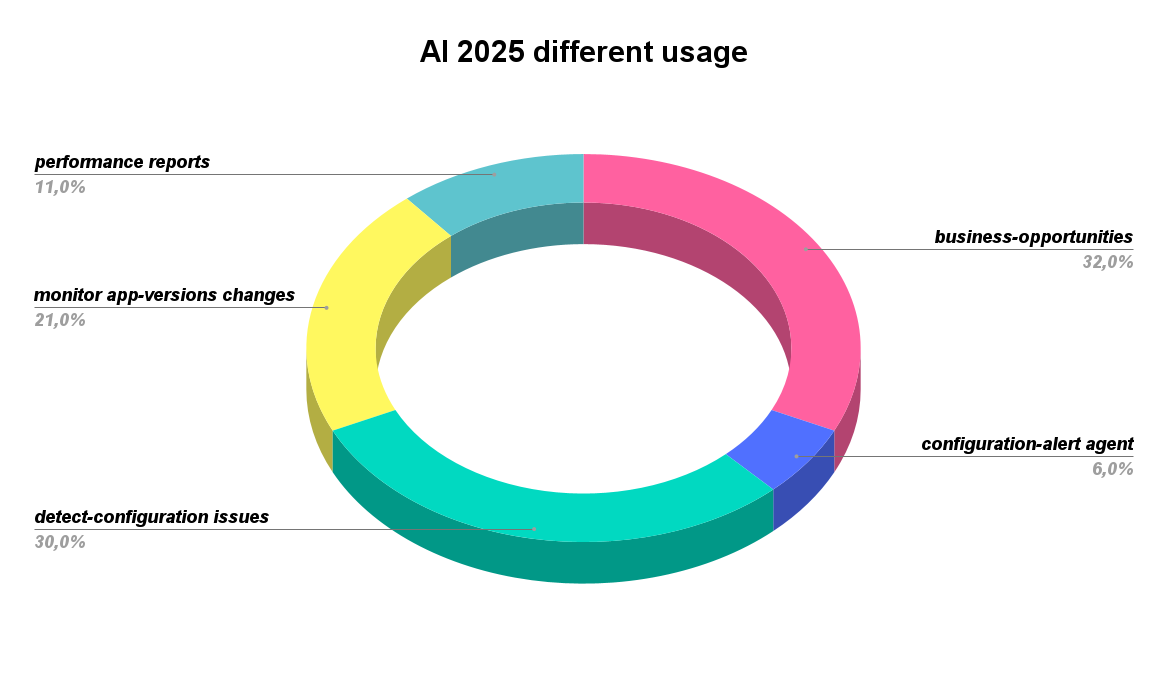

The collected data show that AI is often applied as a virtual data engineer—tasked with safeguarding data quality before strategic decisions are made: 57% of active AI agents focus on functionalities like detecting configuration issues, validating integrations, and ensuring data processes analysis to deliver reliable results.

At the same time, the growing adoption of business optimization agents signals a clear intent to move beyond basic automation and toward performance-driven use cases such as spend allocation, ROAS optimization, and portfolio management.

When examining app categories, distinct priorities emerge. Gaming marketers, who often have advanced data capabilities, act as “Profit Maximizers,” with 57% of their AI interactions focused on efficiency, margins, and expenditures constraints to grow internal revenues. Retail and fintech marketers, in contrast, behave as “Growth Hunters” directing roughly 37% of AI queries toward volume, traffic, and market share expansion. These patterns illustrate that AI usage is highly context-dependent, aligning with each vertical’s business objectives, risk tolerance, and competitive pressures.

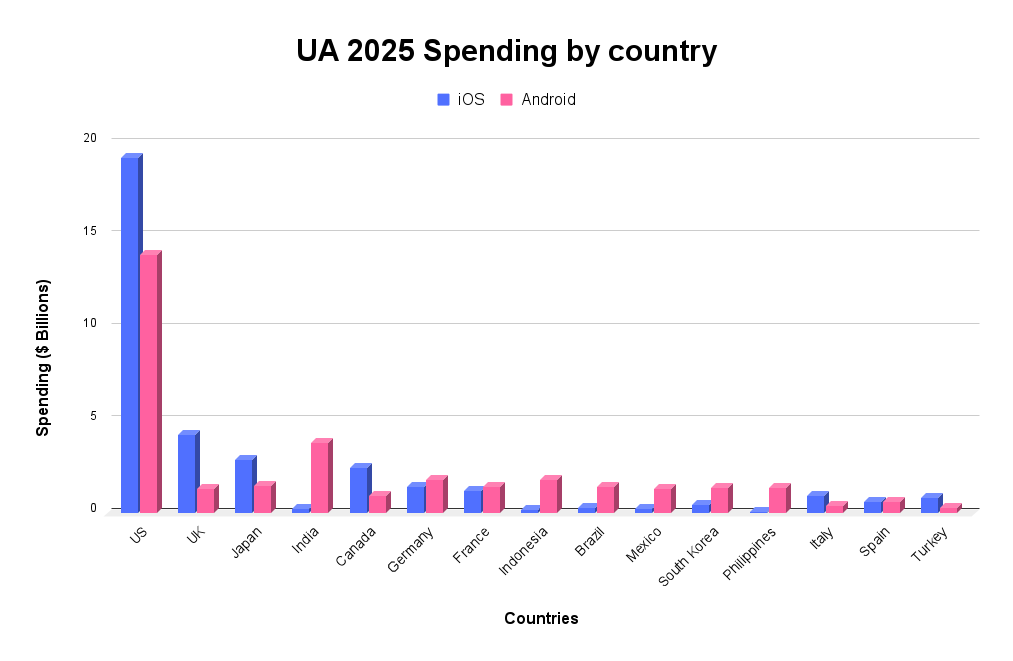

In 2025, global user acquisition (UA) spend hit $78 billion, marking a 13% increase year-over-year, driven almost entirely by iOS, which saw a 35% jump, while Android remained largely flat with -1% of change in user acquisition spend.

Non-gaming apps have been the primary source of growth, climbing 18% to $53 billion, with shopping apps leading the charge—overall spend grew 70%, and iOS spend spiked with over 100% increase, fueled largely by China-based eCommerce companies expanding into Western markets. Betting and casino apps also jumped up, with 127% YoY growth, highlighting strong returns in regulated markets.

Gaming UA spending, counting an increase of YoY of $25 billion, saw more controlled gains, specifically 6% on iOS and 2% Android and reflecting a more disciplined and predictable investment strategy.

Geographically, Europe emerged as the fastest-growing region. Spain and Italy, respectively with 157% and143%, saw triple-digit YoY growth, immediately followed by UK increase up to 92% with share gains ranging from 35% to 50%.Germany and France recorded a reduced YoY growth with strong share gains. The US continued to expand its already dominant position, growing 40% on iOS and 19% on Android, whereas several Android-heavy markets—Brazil, India, and Mexico—lost share, highlighting a strategic shift toward higher-value audiences rather than volume aimed economic models.

Last but not least, emerging categories are reshaping UA spend. Generative AI apps, particularly on Android, are among the fastest-growing segments, driven by demand for creative and productivity tools, signaling that AI-powered technology has become a crucial aspect in each of the two dominant platforms.

We can't conclude this report without analysing the data that delineated paid installs trends during this year.

Paid app downloads in the iOS platform increased exponentially, showing remarkable YoY gains in both western and eastern markets. Having a deeper focus on Western areas, where installations increased from 25% to 84%, Shopping and Finance apps occupy a special place of dominance across the wide range of apps categories.

Non-Western areas are characterised by even a higher increase of paid installations: statistics in fact shows that in those markets the increment of 105%, which means more than doubled the amount of paid installs.

On the contrary, Android displays a pattern decisively more focused on the opposite side of the market. In fact, Western areas present only pretty low or even negative trends, in this region specifically we find the countries of the US (+8%), UK (+1%), Germany (-1%), Italy (-2%) and Australia (-9%). We find , as mentioned before, definitely better statistics in the Major Non-Western markets which deliver nearly all Android gains at 10% to 55%.

The result is by consequence very clear: Android investments are aimed to grow the amount of paid installs almost entirely in non-Western markets, while Western Android performance stays flat or declines.

Conclusion: 2026 digital market preview

The analysis of 2025 clearly indicates that 2026 will not be defined by incremental change, but by consolidation and strategic refinement.

Advertising Channels: Digital advertising will continue to dominate global spend, with budgets increasingly concentrated on high-performing, data-rich channels such as social media, retail media, and short-form video. Traditional media will further lose relevance as marketers prioritize measurable performance, creative agility, and audience precision.

AI Usage: Artificial intelligence will transition from a support tool to a core operational engine. As trust in AI-driven insights grows and data infrastructures mature, 2026 will likely mark the shift toward semi-autonomous and autonomous marketing systems. Marketers will evolve into strategic architects—setting objectives, governance frameworks, and risk thresholds—while AI agents execute optimization, allocation, and scaling decisions in real time.

UA Spending: From a user acquisition perspective, growth will persist, but efficiency will become the primary competitive lever. Rising media costs, creative saturation, and app proliferation will intensify competition for user attention. Investment strategies will increasingly favor platforms that reward engagement and creative excellence, with short-form video emerging as the dominant growth channel.

Paid installs: At the same time, geographic divergence will deepen: iOS will remain the primary driver of value in Western markets with a stronger focus on retention and lifetime value, while Android will fuel user volume growth in non-Western and emerging economies.

To sum up, the key insight to remember is that 2026 will reward companies that balance automation with strategy, scale with efficiency, and growth with sustainability. Those able to integrate AI intelligently, adapt channel mix dynamically, and align acquisition efforts with regional market realities will be best positioned as a leader during the next phase of the digital economy.